.png)

가족 행복의 기반: 금융 안정성

오늘날 불확실한 경제 환경에서 가족의 금융적 미래를 보장하기 위해서는 일상적인 계획 이상의 것이 필요합니다. 최근 통계는 우리의 주의와 행동이 필요한 우려스러운 현실을 보여줍니다.

한국 가정의 숨겨진 취약성

남성 사망자의 16.1%가 60세 이전에 사망한다는 사실을 알고 계셨나요? 이 비율은 같은 연령대 여성 사망자에 비해 2배 이상 높습니다. 가족의 생계부양자가 갑자기 없어질 때, 금융적 영향은 devastating합니다:

- 월 가계소득이 절반 이상 감소 (598만원에서 245만원으로)

- 한국의 가계부채는 지난 20년 동안 GDP 대비 54.4%에서 84.4%로 증가

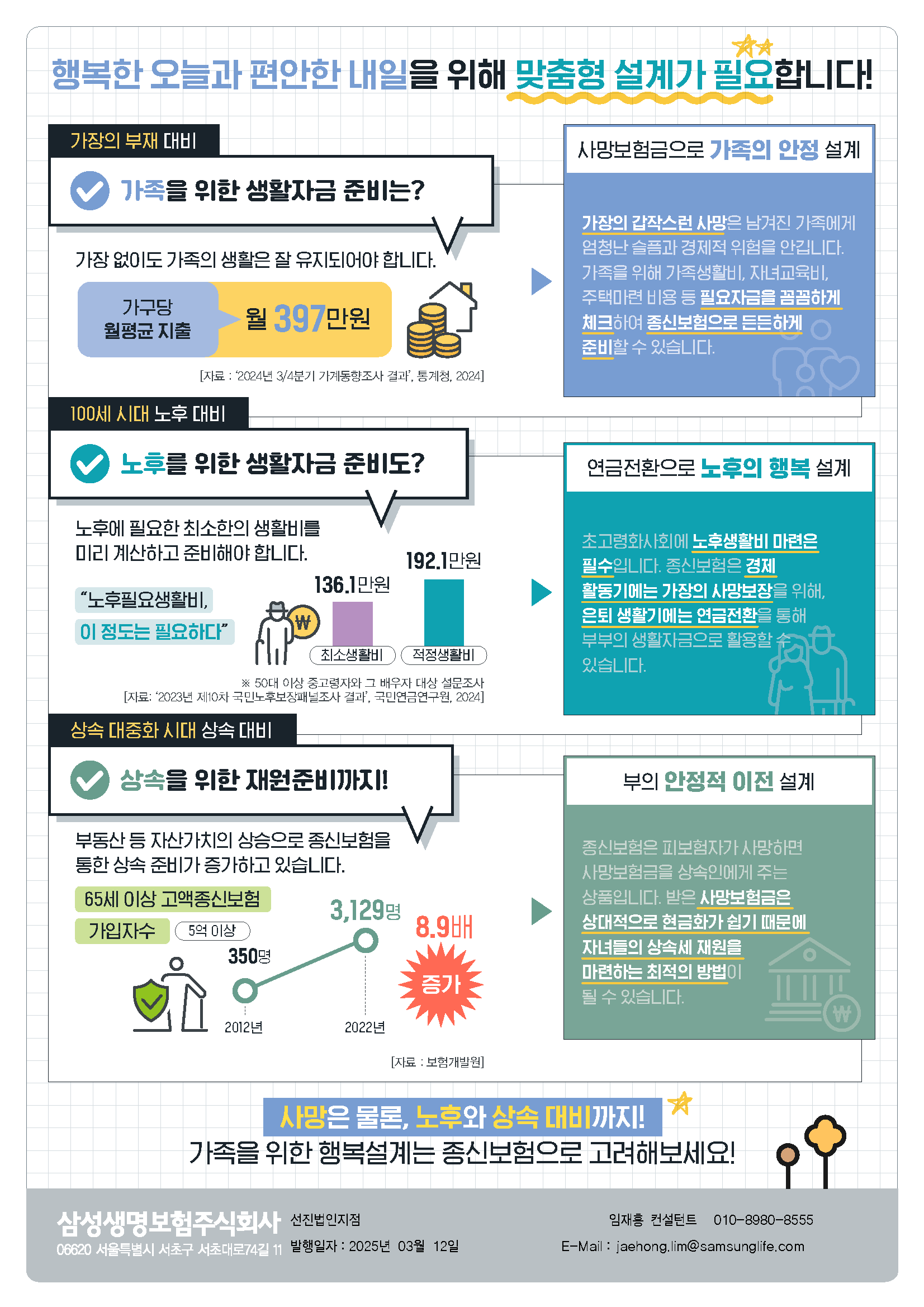

- 평균 한국 가정은 월 397만원을 지출

이 통계는 단순한 숫자가 아니라, 슬픔의 시기에 재정적 어려움을 겪는 실제 가족들을 대표합니다.

가족 금융 안정을 위한 3차원 접근법

1. 오늘의 가족 생활방식 보호

금융 안전망을 설계할 때 가장 큰 관심사는 가족의 현재 생활 수준을 유지하는 것입니다. 종신보험은 즉각적인 보호를 제공하여, 가장의 부재 시에도 가족이 월 약 397만원의 지출을 중단 없이 충족할 수 있도록 합니다.

2. 100세 시대의 노후 보장

고령화 사회인 한국에서 노후계획은 새로운 도전에 직면해 있습니다. 국민연금연구원의 설문 데이터에 따르면 노인들은 다음과 같은 금액이 필요하다고 예상합니다:

- 최소 생활비로 월 136.1만원

- 편안한 생활을 위해 월 192.1만원

종신보험은 근로 시기에는 사망보장을 제공하고 은퇴 시기에는 연금 수입으로 전환할 수 있는 옵션을 제공함으로써, 노후 생활에도 금융적 안정성을 창출합니다.

3. 전략적 자산 이전 계획

상속의 대중화가 우리 눈앞에서 일어나고 있습니다. 65세 이상 고액 종신보험(5억원 이상)은 지난 10년간 8.9배 증가했습니다 - 2012년 350명에서 2022년 3,129명의 보험 가입자로.

왜 이런 급증이 일어났을까요? 종신보험은 자산 이전에 간소화된 솔루션을 제공합니다:

- 사망보험금은 수익자에게 직접 지급됩니다

- 보험금의 유동적 특성은 상속인들이 상속세 의무를 관리하는 데 도움이 됩니다

- 다음 세대에게 자산을 이전하는 체계적인 접근법을 제공합니다

종신보험의 전략적 이점

종신보험이 왜 강력한 재무 계획 도구인지는 여러 인생 단계를 아우르는 다용도성에 있습니다:

- 근로 시기: 가족의 금융 안정성을 보장하는 중요한 보호를 제공

- 은퇴 시기: 지속 가능한 소득을 위한 연금 전환 옵션 제공

- 유산 계획: 세금 혜택과 함께 효율적인 자산 이전 메커니즘 창출

가족의 금융 안정을 위한 행동

현실은 명확합니다—가족의 금융 안정은 삶의 불확실성을 고려하면서 미래 목표를 향해 나아가는 포괄적인 계획이 필요합니다. 맞춤형 종신보험 전략은 이러한 기반을 마련하여 가족이 오늘의 행복을 유지하면서 내일을 위한 안정성을 구축할 수 있게 합니다.

가족의 금융적 미래를 우연에 맡기지 마세요. 귀하의 특정 요구와 목표에 맞는 맞춤형 가족 금융 안정 계획을 어떻게 만들 수 있는지 논의하기 위해 저에게 연락하세요.

통계청(2024), 국민연금연구원(2024), 보험개발원의 데이터에 근거함.

Financial Security: The Foundation of Family Happiness

In today's uncertain economic landscape, securing your family's financial future requires more than just day-to-day planning. Recent statistics reveal a concerning reality that demands our attention and action.

The Hidden Vulnerability of Korean Families

Did you know that 16.1% of male deaths occur before age 60? This rate is more than double compared to women in the same age group. When the family breadwinner is suddenly absent, the financial impact is devastating:

- Monthly household income drops by more than half (from ₩598 million to ₩245 million)

- Household debt in Korea has increased from 54.4% to 84.4% of GDP over the past 20 years

- The average Korean household spends ₩3.97 million monthly

These statistics aren't just numbers—they represent real families facing financial hardship during times of grief.

A Three-Dimensional Approach to Family Financial Security

1. Protecting Today's Family Lifestyle

When designing a financial safety net, the primary concern is maintaining your family's current standard of living. Whole life insurance provides immediate protection, ensuring that even in your absence, your family can meet their monthly expenses of approximately ₩3.97 million without disruption.

2. Securing Retirement in a 100-Year Life Society

Korea's aging population faces new challenges in retirement planning. Survey data from the National Pension Research Institute shows that seniors estimate needing:

- ₩1.36 million monthly for minimum living expenses

- ₩1.92 million monthly for comfortable living

Whole life insurance uniquely addresses this challenge by providing death protection during working years and the option to convert to annuity income during retirement years, creating financial stability throughout life's later chapters.

3. Strategic Wealth Transfer Planning

The democratization of inheritance is happening before our eyes. High-value whole life insurance policies (over ₩500 million) for individuals 65+ have increased by 8.9 times in the past decade—from 350 policyholders in 2012 to 3,129 in 2022.

Why this surge? Whole life insurance offers a streamlined solution for wealth transfer:

- Death benefits are paid directly to beneficiaries

- The liquid nature of insurance proceeds helps heirs manage inheritance tax obligations

- It provides a methodical approach to transferring assets to the next generation

The Strategic Advantage of Whole Life Insurance

What makes whole life insurance such a powerful financial planning tool is its versatility in addressing multiple life stages:

- During working years: Provides critical family protection ensuring financial stability

- During retirement: Offers pension conversion options for sustainable income

- For legacy planning: Creates efficient wealth transfer mechanisms with tax advantages

Take Action for Your Family's Financial Security

The reality is clear—family financial security requires comprehensive planning that accounts for life's uncertainties while building toward future goals. A customized whole life insurance strategy creates this foundation, allowing your family to maintain happiness today while building security for tomorrow.

Don't leave your family's financial future to chance. Connect with me to discuss how we can create a personalized family financial security plan tailored to your specific needs and goals.

Based on data from Statistics Korea (2024), National Pension Research Institute (2024), and Korea Insurance Development Institute.